Property tax myths and misunderstandings

Myth 1: Assessors determine property taxes

Typically property tax rates are set by school boards, town boards, village boards, and county legislatures, but not by assessors. Each board determines the total amount of taxes it needs to raise, and then divides that number by the total taxable assessed value of the jurisdiction to determine the tax rate. Your share of the tax is calculated by multiplying the tax rate by your property's assessed value minus exemptions, such as STAR.

Assessors are responsible for determining your property's assessed value. In order to do this, the assessor estimates your property's market value (the price it would sell for in the real estate market), and then applies the municipal level of assessment (LOA) to that market value. In many communities, the level of assessment is 100 percent, so a home with a market value of $90,000 has an assessed value of $90,000. In a town with a level of assessment of 50 percent, the assessed value of the same home is $45,000.

The assessor also performs other functions, such as processing exemption applications and keeping track of the local real estate market, but the assessor does not determine your tax rate.

Learn more about the job of The assessor.

Myth 2: Taxes are high because of assessments

It is important to distinguish between taxes and assessments. If you feel your taxes are too high, you should take that up with the town board, school board, or other governing authority that is determining tax levies and setting the tax rates. If you feel your assessment is too high, there are administrative and judicial processes where you can seek to have your assessment lowered.

Assessments should be based on market value, and if you feel your assessment is too high, your first step in confirming that is to determine your property's market value. The best way to do this is to look at the sale prices of similar properties in similar neighborhoods.

If you still feel that your assessment is too high, we recommend that you informally discuss your concerns with your assessor. More information on the grievance process is available from your assessor's office.

Myth 3: NY State collects too much money through property taxes

While New York State government receives no money from the real property tax, this stable revenue source is vitally important to the delivery of services to the state's citizens. Local governments and school districts collect the property tax, which is their largest source of revenue. That's one of the main reasons that property taxes and assessments are administered locally (rather than by the state) in New York.

Myth 4: Equalization rates can correct unfair assessments

Equalization rates are determined by the State Office of Real Property Tax Services and represent the overall ratio of a municipality's total assessed value to the municipality's total market value. Because equalization rates are municipal wide measures, they are not intended to correct unfair individual assessments in a city or town. The assessor has the primary role in ensuring the fairness of individual assessments, subject to the right of owners to seek administrative and judicial review of assessments.

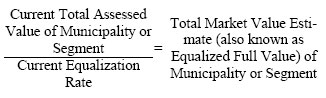

While equalization rates have many uses, they are most commonly known for their use in apportioning property taxes among municipal segments of school districts and counties. In order for a school district or county to fairly distribute its property tax levy (the total amount of taxes to be collected), the levy needs to be divided in proportion to the total market value of each municipality or municipal segment. This allows for an equitable distribution of taxes based upon the market value of each municipality or segment.

In the apportionment process, the equalization rate is used to estimate the total market value of an entire municipality and/or segments of municipalities. The formula used for this calculation is:

Myth 5: Tax rates are good indicators of tax increases

In late August, as the date for mailing school tax bills approaches, the tendency is to compare the tax rate for the previous year with the tax rate for the current year. In fact, tax rates are not accurate indicators of how much more a school district is collecting in taxes this year. For that, you need to look at the tax levy.

Tax rates are misleading because they are based on the aggregate assessments of each municipal segment in the school district. If one city or town in the district has done a reassessment that year, that segment's tax rate may drop drastically. Put another way, a municipality might increase assessments and the school could keep the tax rate the same and it would still collect more taxes.

If you want to know if the school district, city, town, or county is spending more, look at the budget. If you want to know if it's collecting more in taxes, look at the levy.

Myth 6: A cap on assessments would lower property tax burdens

Occasionally, a proposal is made to cap assessment increases at a certain percentage each year. Doing so would result in some property owners paying less than their fair share of taxes, while their bills are subsidized by other homeowners. Eventually, properties that are increasing in value more quickly would be underassessed, while properties that are not increasing in value as quickly would be subsidizing the underassessed property's taxes. (Typically, in the case of residential properties, lower-valued homes increase in value slower than higher-valued homes.)

Meanwhile the town, county and school district would continue to collect the same amount of taxes that they would if assessments weren't capped. A cap on assessments doesn't result in less taxes being collected, it just redistributes the tax burden to the disadvantage of properties increasing in value more slowly.

Myth 7: I have to be 65 to get the STAR exemption

All New Yorkers who own and live in their one-, two-, or three-family home, condominium, cooperative apartment, mobile home or farm home are eligible for the Basic STAR tax cut on their primary residence. There are no age or income limitations with Basic STAR.

Seniors with incomes not exceeding the statewide standard may be eligible for the Enhanced STAR exemption. Applicants need only be 65 years of age as of December 31 of the year in which the exemption will begin. If you think you may be eligible, please contact your assessor for more information.

Myth 8: The STAR exemption is ending

The STAR program does not have a sunset (or expiration) date. In other words, NYS homeowners will continue to benefit from STAR unless the Legislature votes to end it.