Customer Loyalty Cards

Tax Bulletin ST-145 (TB-ST-145)

Issue Date: September 29, 2011

Introduction

Many businesses use loyalty cards to offer incentives to frequent customers. Some loyalty cards provide discounts at the time of purchase, while others provide incentives through an accumulation of points that the customer can redeem at a later date. For sales tax purposes, these discounts are treated the same way as discounts provided by paper coupons.

This bulletin explains:

- how sales tax applies to the price of discounted items purchased using loyalty cards, and

- the steps businesses must take to ensure:

- that customers are informed of the types of discounts received using a loyalty card; and

-

proper recordkeeping and reporting of taxes due on the discounted prices of items purchased using loyalty cards.

Types of loyalty card discounts

Drug stores, grocery stores, and other retail establishments often offer discounts on items in their stores if the customer provides the cashier with a loyalty card at the time of checkout. Some discounts are provided by the store itself, while others are manufacturers' discounts. The taxability of these discounted items differs according to the type of discount being given.

Manufacturer's discounts

Manufacturer's discount means the manufacturer of an item reimburses the store for selling the item at a discount. Sometimes the store is reimbursed by a third party instead of a manufacturer. Third party reimbursements to the store are treated the same as a manufacturer's discount.

A manufacturer's discount is often identified by a store using the word Manufacturer's or an abbreviation of Mfr. to show that the discount is a manufacturer's promotion.

When a manufacturer's discount applies, sales tax is due on the full price of the item, not on the discounted price. Since the seller will receive reimbursement from the manufacturer for the amount of the discount, the actual selling price is not reduced, even though the amount paid by the purchaser is reduced.

Example 1: A store sells a taxable item for $1. The item is eligible for a 25-cent manufacturer's discount if the customer presents a loyalty card at checkout. The store must collect tax on the full price of $1 since the store will still receive $1 in total, 75 cents from the customer, and 25 cents from the manufacturer. The tax (assuming a rate of 8%) and amount due from the customer are computed as follows:

| Selling price of the item: | $1.00 |

| Sales tax (.08 x $1.00): | .08 |

| Subtotal: | $1.08 |

| Less amount of the manufacturer’s discount: | - .25 |

| Amount due from customer: | $ .83 |

Store discounts

A loyalty card may also give the customer a store discount. Unlike a manufacturer's discount, a third party doesn't reimburse the seller for the amount of the discount. As a result, the payment received by the seller is reduced, and tax is calculated on the reduced price.

Example 2: A store sells a taxable item for $1. The item is eligible for a 25-cent store discount if the customer presents a loyalty card at checkout. The seller only receives 75 cents for the item and the tax is due on that amount. The tax (assuming a rate of 8%) and amount due from the customer are computed as follows:

| Selling price of the item: | $1.00 |

| Less amount of the store discount: | - .25 |

| Subtotal: | $ .75 |

| Sales tax (.08 x $.75): | .06 |

| Amount due from customer: | $ .81 |

Combination discounts

When a loyalty card gives a customer a combination of a manufacturer’s discount and a store discount, the tax is computed on the cost of the item, less the store discount.

Example 3: A customer purchases an item for $15.00. The item qualifies for a $2.00 manufacturer's discount and a $1.00 store discount. The tax rate is 8%. The tax and amount due from the customer are computed as follows:

| Selling price of the item: | $15.00 |

| Less amount of the store discount: | - 1.00 |

| Subtotal: | $14.00 |

| Sales tax (.08 x $14.00): | 1.12 |

| Subtotal: | $15.12 |

| Less amount of the manufacturer’s discount: | - 2.00 |

| Amount due from customer: | $13.12 |

Future discounts

Certain loyalty cards allow a purchaser to accumulate points for future discounts. Some cards earn free merchandise, while others offer discount coupons that are mailed to customers.

The taxability of these future discounts also depends on whether or not the seller receives reimbursement from a third party, such as a manufacturer:

- If the seller is reimbursed for the discount, sales tax is due on the full price, without regard to the discount.

- If the seller is not reimbursed for the discount, sales tax is due on the discounted price.

Example 4: A customer enters a fast food restaurant and orders a $5 sandwich and a $2 bottle of soda. The cardholder has accumulated enough points to have earned a free sandwich.

If the restaurant is not reimbursed for the cost of the sandwich by a parent corporation or other third party, the seller would collect tax only on the $2 price of the soda. The sales tax (assuming a rate of 8%) and the amount due from the customer are computed as follows:

| Selling price of the meal: | $7.00 |

| Less amount of the store discount for free sandwich: | 5.00 |

| Subtotal: | $2.00 |

| Sales tax (.08 x $2.00): | .16 |

| Amount due from customer: | $2.16 |

Third-party seller discounts

Occasionally a store offers a loyalty card incentive that allows for discounts on purchases from third-party sellers. If the third-party seller is being reimbursed by the store that issued the loyalty card, the loyalty card discount is taxed as a manufacturer’s discount when a purchase is made from the third-party seller. This is because the third-party seller is still receiving the full selling price for its product, part from the customer and the balance from the card issuer.

Example 5: A supermarket chain offers a program where for every $50 in groceries purchased, the customer can earn 10¢ off per gallon of gas at a specific gas station chain. Customers receive the discount on gas by swiping their supermarket loyalty card at the gas station pump. The supermarket chain reimburses the gas station for the amount of the discount given to the customer.

Because the gas station is still receiving the full pump price for the gas, the discount is taxed in the same manner as a manufacturer’s discount. As a result, the gas station must collect sales tax from the purchaser based on the full selling price. The state tax would be collected on a cents-per-gallon basis and the local tax on either a cents per-gallon basis or at a percentage rate, depending on the locality where the sale takes place.

Proper disclosure of the type of discount that applies

As discussed above, use of the word Manufacturer’s or the abbreviation Mfr. informs the customer that a manufacturer's discount applies to a sale. As a result, the sales tax must be computed on the full price of the item, not the discounted price.

However, when using a loyalty card at checkout, it may not be clear to a customer what type of discount applies. If the seller fails to properly disclose to the customer that the discount given is a manufacturer's discount:

- the seller must collect sales tax from the customer on the reduced price of the item; and

- the seller is liable for and must pay sales tax on the difference between the full selling price of the item and the reduced price charged to the customer. That means the seller itself will owe the tax due on the amount of the discount.

The seller must report and remit the sales tax on the amount of the discount, along with the tax collected from the customer, on the seller’s sales and use tax return.

To avoid this liability for sales tax due on the amount of a manufacturer's discount, a seller must advise its customers that some loyalty card discounts are manufacturer's discounts, while others are store discounts. To do this, a seller should:

- identify items subject to a manufacturer's discount using Manufacturer’s or Mfr. on its coupons, in its in-store circulars, and in its newspaper advertisements;

or

- use store shelf tags that:

- are distinguishable from a standard shelf tag, based on their size, color and wording; and

- indicate by Manufacturer's or Mfr. printed on the tag that the discount is a manufacturer’s discount;

or

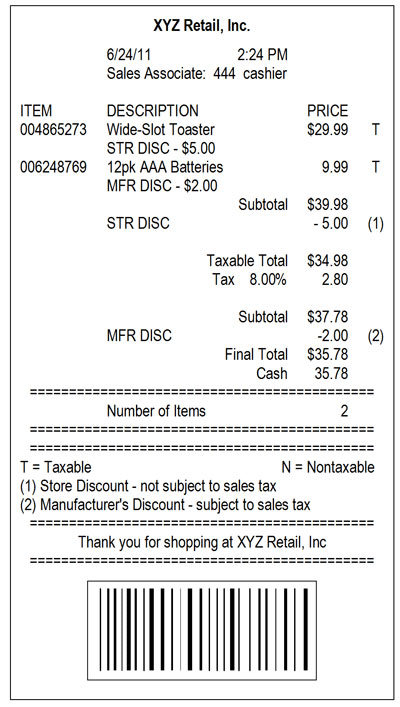

- post signs near its checkout registers advising customers that some loyalty card discounts are manufacturer’s discounts while others are store discounts, and program its cash registers to note on the customer's receipt which discounts given are taxable manufacturer’s discounts, and which are exempt store discounts. For example, a seller's sign could read:

"A discount offered under our [insert name of program] may be a store discount, a manufacturer’s discount, or a combination of both. The type of discount given on the purchase of an item will be indicated on your receipt. A manufacturer's or other third-party discount will be designated as Manufacturer's or Mfr."

Such a receipt might look something like this:

Note: A Tax Bulletin is an informational document designed to provide general guidance in simplified language on a topic of interest to taxpayers. It is accurate as of the date issued. However, taxpayers should be aware that subsequent changes in the Tax Law or its interpretation may affect the accuracy of a Tax Bulletin. The information provided in this document does not cover every situation and is not intended to replace the law or change its meaning.

References and other useful information

Tax Law: Section 1101(b)(3)

Regulations: Sections 526.5 and 528.27

Memoranda:

TSB-M-11(10)S, Tax Department Policy on Manufacturer's Discounts Received Using Store Loyalty Cards

Bulletins:

Coupons and Food Stamps (TB-ST-140)

Taxable Receipt (TB-ST-860)